Old Glory Bank's unification of traditional banking and cryptocurrency.

We have announced our plans to bring together legacy finances and future currency technology in one dashboard.

Cryptocurrency and stablecoins are the culmination of everything we have been fighting for - the Privacy, Security, and Liberty you and your finances deserve.

Old Glory Bank's Next-Gen Banking

We believe we will be one of the first financial institutions to unite crypto with daily banking.

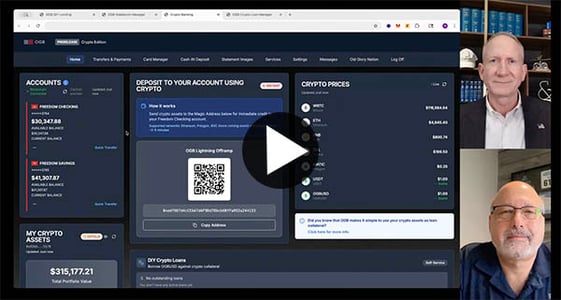

In this demo, our Chief Innovation Officer, Michael Staw, and President and CEO, Mike Ring, share an exciting update on our plans to offer customers the ability to manage your crypto and stablecoins, a self-custodial wallet, and your traditional bank accounts within a single dashboard.

Please watch our latest demo video and share it with your friends and colleagues who are as excited as we are about the next generation of finance.

Freedom to Choose

At Old Glory Bank, we see the evolution of banking – the incorporation of cryptocurrency, stablecoins, and self-custodial wallets – as the culmination of everything we have been working for: your Privacy, Security, and Liberty in banking.

Your freedom to choose between traditional banking and legacy currency, and digital currency is part of that autonomy. Many of you have been eager for this merger of old and new, and it's finally here.

Others of you have no interest in crypto and digital currency, and that's ok, too. We will continue to offer both, so that your liberty is protected. We stand with you.

Watch the Demo

We believe Old Glory Bank will be the first bank to easily link your crypto, stablecoins, and self-custodial wallet into a single dashboard, combined with your OGB Accounts. Once linked, you can easily “on-ramp” and “off-ramp” US Dollars (fiat) with popular crypto coins, creating a seamless experience to spend fiat and crypto every day.

OGB Customers will be able to use our new stablecoin, OGBUSD, for payments and remittances around the world. Recipients can hold it, spend it, exchange it for U.S. dollars at Old Glory Bank, or convert it on any exchange supporting ERC-20 standard tokens.

OGBUSD will be backed by US Dollars, 1 to 1, so you will always know the value and buying power.

Cryptocurrency 101: Terms to Know

Crypto fans and experts, you can skip to the next section.

If you are just learning about crypto, you might find this glossary helpful.

Cryptocurrency

A type of digital money. Unlike dollars, it doesn’t exist in physical form and isn’t controlled by a government or bank. Instead, it’s powered by blockchain technology.

Popular cryptocurrencies include:

- Bitcoin (BTC) – the first and most well-known

- Ethereum (ETH) – used for smart contracts and NFTs

- Solana, Cardano, Dogecoin – other coins with different purposes

You can use crypto to buy things, invest, or even support creators online.

Stablecoin

A type of digital currency that is pegged to the value of a stable asset, such as a fiat currency like the U.S. dollar. Its purpose is to combine the benefits of cryptocurrency, like fast, borderless transactions, with the price stability of traditional money.

Old Glory Bank plans to mint our own stablecoin, OGUSD, with the release of our crypto features in early 2026.

Fiat

Government-issued currency that is not backed by a physical commodity, like gold or silver, but rather by the government's declaration that it has value. Examples include the U.S. dollar (USD) or euro (EUR).

When used in digital finance, fiat currency typically refers to traditional money that can be transferred electronically, such as through bank apps, payment platforms, or converted into stablecoins.

Key

A crypto key is a fundamental part of how cryptocurrencies and blockchain technology work. It's a piece of cryptographic information used to secure, access, and control digital assets.

A private key is a string of letters and numbers used to sign transactions and prove ownership of a crypto wallet. It must be kept secure and never shared - sharing your private key is like handing your actual physical wallet to a crook and inviting them to clean out your cash.

A public key is derived from your private key using cryptographic algorithms. It can be shared with others safely, often to allow you to receive cryptocurrency.

Think of your public key as your email address (you can share it) and your private key as your email password and PIN (you must keep it secret).

Gas

In cryptocurrency, gas refers to the fee required to perform a transaction or execute a smart contract on a blockchain network. The gas fee is the amount of cryptocurrency you must pay to process your transaction. The amount of gas required depends on the complexity of the transactions, the congestion of the network, and the price of the gas itself.

Blockchain

A digital ledger – a record of transactions – that is:

- Decentralized: No single person or company controls it

- Transparent: Everyone can see the history of transactions (but not your identity)

- Secure: Once something is written, it can’t be changed

Blockchain works by keeping the record of transactions across a decentralized and encrypted network of computers, so the data is secure, verified, and permanent.

Token

A digital asset issued on a blockchain. This can represent currency, ownership, or access rights.

On-ramp and off-ramp

In the context of cryptocurrency, on-ramps and off-ramps refer to the services and platforms that allow users to move between traditional currencies ("fiat" such as US dollars) and digital assets (like Bitcoin or Ethereum).

An on-ramp is a service that lets you buy cryptocurrency using fiat currency. It's your entry point into the crypto world. An off-ramp is a service that lets you convert cryptocurrency back into fiat currency.

DeFi

Short for Decentralized Finance, DeFi refers to a movement within the cryptocurrency space that aims to recreate and improve traditional financial systems – like lending, borrowing, trading, and investing – using blockchain technology and smart contracts, without relying on centralized institutions.

Key features:

- No intermediaries: Transactions are peer-to-peer, governed by code instead of companies or governments.

- Smart Contracts: Automated agreements that execute when predefined conditions are met, such as a transaction or event.

- Open Access: Anyone with a crypto wallet can participate without credit checks or paperwork.

- Transparency: All transactions are recorded on public blockchains. Your identity is private, but your transaction is recorded and verified.

Self-Custodial Wallet

Also known as a non-custodial wallet, this is a type of cryptocurrency wallet that gives users full control over their private keys and digital assets stored on a blockchain network.

Unlike custodial wallets, such as those offered by and controlled by crypto exchanges, no third party holds your keys. This means that only you can access and manage your funds. Self-custodial wallets typically do not require you to share your personal data, so your privacy is protected. With direct blockchain access, you can interact directly with decentralized applications and platforms ("DeFi").

Smart Contract

A self-executing program stored on a blockchain that automatically enforces the terms of an agreement when predefined conditions are met. It is the digital version of a traditional contract, but without the need for intermediaries like attorneys, banks, or brokerages.

FAQs about Old Glory Bank's Next Generation of Banking

Find answers to Old Glory Bank's specific plans and how we are building our unified dashboard.

Thank you for reaching out. As we describe in our S-4 (OGB DAAQ S-4) filed as part of our intended public listing of our stock on the Nasdaq, we made the commitment to not launch Next Gen Banking until after the consummation of our business combination (described in our S-4). This will ensure we have sufficient capital to launch crypto banking in a safe and sound manner.

Our great unified dashboard, which lets you view your crypto prices and your self-custodial wallet, will be available in phase one. You’ll be able to move money on and off the blockchain, use our stablecoin, and we will have liquidity access lines set up. Phase two will include stablecoin as a service and our custodial wallet.

Please stay tuned for more announcements! We are working as quickly as we can responsibly to launch these and other initiatives.

For today, please use your Old Glory Bank accounts as you always have, and we will let you know when this platform is ready.

Definitely not! We believe in giving our customers the freedom of choice. With Old Glory Bank, you will have the freedom of choice between using traditional bank accounts, crypto, or both.

No, the beauty of our product will be the unity of crypto and daily banking in a single app. Those customers who wish to use only the traditional banking features that you are used to will be able to, and those who choose to use the crypto features can do so as well. Freedom of choice!

The initial launch will support ETH mainnet, Polygon, PulseChain, with the possibility of additional EVM chains. XRP and BTC will be fast followers.

We’re also developing a seamless stablecoin on-ramp and off-ramp that lets you move funds directly to and from your Old Glory Bank account, without the hassle of third-party DEXs or untrusted connections. You will be able to do all of this using either the Freedom Checking or Premium Checking accounts, so please choose the one that fits your needs the best.

OGB will offer crypto exchange services directly in our online banking app, allowing you to trade various crypto assets easily, and across chains.

At launch, we will have wallet linking capability, allowing you to trade from your own non-custodial wallet, and our own custodial wallet solution will launch shortly thereafter.

With regard to ISO20022, there are no such events emitted by OGB crypto transactions.

Finally, with regard to XRP, we use the Ripple Rails for XRP transactions, but other transactions can ride a variety of rails according to need.

The initial launch will support ETH mainnet, Polygon, PulseChain, with the possibility of additional EVM chains. XRP, and BTC will be fast followers.

So, the answer is yes, but not on the initial launch.

The OGUSD stablecoin is backed dollar-for-dollar (i.e., no fractional shares). A dollar-backed stablecoin cannot lose value, except to the extent inflation impacts all US currency. OGUSD is like "cash." A dollar-backed stablecoin makes it easy to remit payments, but we do recognize it is not a hedge against inflation. The purpose of OGUSD is to make payments anywhere in the world and fly over the top of the Federal Reserve and the SWIFT platform. But a stablecoin is not an investment asset and is not a hedge against inflation.

OGUSD is primarily different from a CBDC in that 1) it is not issued by any government or government agency, and 2) there is no centralized government control of it. The key implication is that even though transactions are visible on chain, your ID and its association with your wallet can remain private. In terms of interchangeability, OGUSD is freely tradeable and can always be redeemed at a guaranteed 1:1 through your OGB account. And, as an ERC-20 token, you may swap it with other tokens on exchanges or through our interface at very low swap fees.

Lastly, the bank does not approve OGUSD transactions. It’s your money. You spend it as you choose.

Our onramp and offramp solutions are designed to move funds to and from fiat, which requires an OGB bank account. Of course, we do have free accounts!

We will have all the advanced security protecting your accounts just as we do today with your traditional bank accounts. With regard to your personal crypto wallet, no one should ever need or want the keys to your wallet, including any bank. So if you choose to use a self-custodial wallet, we have no power to access that wallet whatsoever. The security is well within your control.

When it comes to custodial wallets you have with us, we are working on security protocols now, which will give you the same level of security you expect and deserve from any bank.

Regarding protection against search and seizure or government freezing accounts? We will hold to the same standard we do now, which is pushing the limit to the extent of the Constitution and the law. We are a law and order bank. We frequently push back on subpoenas, and we will not willingly give up a customer’s data. But we will always operate lawfully. When it comes down to it, you have to trust that your bank has your back, knows the law, and isn’t afraid to push back on unlawful overreach.

There is no conversion process or conversion tool. You keep your keys private, and we have no ability to access your crypto account. Thus, even if hacked (which is extremely unlikely given our advanced security protocols), we cannot leak what you have not shared.

We are working on a custodial wallet solution as part of our crypto solution. Our crypto services will be compatible with your cold wallet as well, if you want to go that way.

There is no requirement to use our stablecoin, but we think you’ll want to take advantage of the low friction in using it for on-ramping and off-ramping.

There will be no minimums, but large transactions may require an approval.

Yes, using your custodial wallet, and shortly thereafter, a custodial wallet. If you need treasury services, we have a “treasury management” solution in development that allows a business to hold crypto on its own balance sheet in a custodial wallet at Old Glory Bank. Although our initial launch will not likely have this ready, we predict it will be ready later in 2026.

Old Glory Bank is building a best-in-class crypto experience right inside our online banking platform. Soon, you’ll be able to view your crypto balances and activity alongside your regular accounts, simply by linking your self-custodial wallet to your online banking login. Unfortunately, currently, Old Glory Bank does not have a currency desk and, thus, we are not able to exchange or convert foreign currency. For today, we accept deposits in US dollars, so if your crypto exchange converts crypto into US Currency and ACH's currency to your account, we have no preset restrictions on crypto firms and will look at every transmitter of XRP of funds under the same color lens.

We do not have an announcement regarding gold and silver storage/conversion services at this time.

We know how big the need and opportunity are for crypto-backed lending, and we are currently building our lending solution. This will be incorporated in the second phase of NextGen banking at OGB, coming in late 2026.

For crypto lending, collateral is held by a dedicated collateral contract which will be publicly viewable. Its assets will not be rehypothecated. In the future, we may offer loans in which we rehypothecate collateral, however, that would be a completely separate offering in which the terms are clear, and likely with a different rate structure.

It is indeed on-chain lending, and for accounts that fall within certain automatic approval parameters, it is virtually instantaneous. The rates, limits, and loan-to-value caps will fluctuate in response to market conditions.

These types of loans are asset-backed, as opposed to credit-based.

Self-loans, or liquidity access lines, will be available 24/7 for loans that fall within the auto-approval criteria and will be funded nearly instantly.

Anchorage does not offer public wallet/custody services; they only offer it for corporate treasuries. Regarding treasury services, we will have a GREAT solution, but not on day one. Standby for more information on this coming soon!

Yes, and better. We are a unified fiat and digital solution, so not only will you be able to hold your treasury assets, but you’ll also be able to do everything else that you can with a traditional bank.

Transaction times vary per blockchain. Our demo was running on Sepolia, which like Ethereum Mainnet, where our initial release will be, has a block completion time of 12 seconds, generally speaking. Since blocks complete roughly on that 12-second beat, sometimes a transaction hits the transaction queue right before the block closes, and feels instant, and sometimes it comes right after and must wait nearly 12 seconds for the next block. On a couple of those transactions, we probably got lucky. On internal transactions we generate, we use an optimized gas strategy that is extremely likely to hit the current block in progress, maximizing our chances of “getting lucky.”

On XRPL, you’re going to see reliably fast transactions, given the 3-second block time.

We are a law and order bank, so we are always going to follow the law. When you sell a digital asset, just like when you sell stock or land, you will be issued a 1099, as we are required to report the gross proceeds to the IRS. The solution is to not sell your crypto until you need to, and thus you will not have a taxable transaction.

If you send a stablecoin from one account to another account, that is not a redemption, and that happens within your own self-custodial wallet, so there is no transaction to report.

The cost for using OGB’s custodial wallet is free to customers in good standing. With regard to gas fees, there is no gas fee on transactions that are initiated by the bank on your behalf, which includes things like onramping and offramping (subject to daily limits). Transactions you initiate, or that require your wallet approval, will be subject to gas. For exchanges, we work to get you the best spot price, and we will make the fees visible to you before you confirm the transaction. Stablecoin generation, minting, and burning are likely to be fee-free because OGB is running these transactions from our own wallet, paying our own gas for the transaction.

We will support a very wide range of cryptocurrencies.

Our solution supports all major wallet providers.

Within our app, you can move cash to crypto and back, as well as trade between chains. However, cross-chain swaps will take longer to clear.

Yes!

On and off ramping is easiest through the minting/burning of OGUSD with just a couple of clicks. For other tokens, we onramp and offramp by finding the best available fill price.

The collateral backing OGUSD is USD only. Please note that we may hold some of these assets in overnights and US Treasuries with expirations of 93 days or less, but we guarantee that it is all liquid and USD.

As of today, you will not earn interest on a stablecoin, because if a bank paid interest on the money backing the stablecoin, the bank would have to make money to pay that interest, which means fractional banking and risk. OGB won’t loan out the money backing your OGUSD stablecoin, which means we don’t earn interest on that money, so we can’t pay you interest.

Our stablecoin contract is a derivative of the ERC-20 standard stablecoin contract. To mint OGUSD, it’s just a couple of clicks, and transactions are generally completed within 10-15 seconds.

You can easily redeem your crypto holdings directly into your OGB account. If you need cash, we have a large network of free ATMs available.

We will have a treasury management wallet for business accounts. For example, if you are a company that creates a utility token, you will be able to store your tokens in our secure wallet.

Absolutely! We call this Old Glory Select. “One card, that’s all.” With your OGB Card, you’ll be able to decide for each purchase whether you want to spend fiat (like a debit card), use your credit line (like a credit card), or use your crypto.

Yes, but you don’t have to in order to use our crypto services. Our solution lets you keep your coins where you want. You can either link those crypto accounts to your OGB account or you can use our upcoming custodial wallet to transfer tokens to us.

In either case, you’ll be able to see your integrated balances right alongside your existing account, and both methods will allow you onramp and offramp to OGUSD.

Cryptocurrency vs. CBDC

It is critical to understand the distinction between cryptocurrency and CBDC. It can be easy to confuse the two.

While both operate digitally, the key distinction lies in who controls them and what that means for personal financial autonomy.

On January 23, 2025, President Trump issued an executive order entitled “Strengthening American Leadership in Digital Financial Technology.” In this order, he set out “five high-level policy objectives:

- Protecting the lawful use of blockchain networks, participation in mining and validation, and self-custody of digital assets without unlawful censorship;

- Promoting dollar-backed stablecoins;

- Ensuring fair and open access to banking services;

- Providing “regulatory clarity” for digital assets based on “well-defined jurisdictional regulatory boundaries,” and

- Prohibiting Central Bank Digital Currencies (“CBDC”).

So, what’s the difference?

CBDCs vs. Cryptocurrencies: Who Controls Your Money?

CBDCs are government-backed digital currencies issued by central banks, while cryptocurrencies operate on decentralized networks. Supporters of CBDCs argue they improve efficiency and security, while critics warn they could lead to increased government control over individual financial freedom. On the other hand, cryptocurrencies offer a free-market alternative, though they come with their own risks and volatility.

Ultimately, the decision of whether to embrace or reject either system should be left to the individual investor – not dictated by the state.

Old Glory Bank has always taken the position that CBDCs are not likely to be implemented in the United States of America as the Federal Reserve cannot designate digital currency as "legal tender" under Section 31 U.S.C. 5103. Digital Dollars would be outside what Congress intended when it enacted this statute, especially considering the history of this statute back to 1884. Fortunately, the current chairman of the Federal Reserve also shares our view and already acknowledged on March 20, 2021, that the Federal Reserve could not issue digital currency without Congress enacting legislation. In this regard, we do not believe that a Republican House or the Senate will support this legislation. Of course, this position was even before President Trump’s express Executive Order prohibiting CBDC which further makes it apparent that a CBDC is neither likely nor possible in the United States.